Funding considerations

As the plan sponsors, Ontario Teachers’ Federation (OTF) and the Ontario government must consider a range of factors and risks when considering the long-term financial health of the plan.

$31.2B

preliminary funding surplus

11%

average contribution rate per plan sponsor

100%

inflation protection on all pensions

As the plan sponsors, Ontario Teachers’ Federation (OTF) and the Ontario government must consider a range of factors and risks when considering the long-term financial health of the plan.

The pension plan continues to evolve to meet changing economic and demographic factors. A record of changes in contribution rates, pension benefits and inflation protection levels can be found below, along with a summary of decisions made to address funding shortfalls or surpluses since the pension plan became an independent entity in 1990.

A: Yes, your pension is safe and secure.

The Ontario Teachers’ Pension Plan Board (Ontario Teachers’) is well positioned to navigate an uncertain and unpredictable investment and geopolitical environment. By adapting to changing market conditions while keeping a long-term perspective and focusing on partnering with businesses and management to create value and ensure success across our global portfolio, Ontario Teachers’ works to continue to deliver on their mission of delivering outstanding service and retirement security for you over the long term.

A: Members can rest assured that there is no current impact on pension payments. Retired members will continue to receive pension payments as scheduled. Your basic pension income is based on your earnings and years of service in the plan and is not impacted by the investment returns of the plan. In addition, as the Plan is fully funded, the January 1, 2026 increase to pensions in pay for all pension credit will remain at 100% of the Consumer Price Index (CPI) Ratio (see below for further details).

Also, with the decision to file the January 1, 2025 valuation, there will be stability in contribution and benefit levels at least until the next valuation is filed. The next required funding valuation filing is as at January 1, 2028, although the sponsors may choose to file at an earlier date.

A: Classifying the surplus as a contingency reserve is beneficial for plan members because it facilitates greater stability of contribution rates and benefit levels in case a future filed funding valuation shows a decline in assets or an increase in pension costs.

It is aimed at keeping the plan fully funded with “base provisions” as referred to in the Funding Management Policy (FMP) – meaning an average contribution rate of 11% and full inflation protection on all pension credit.

A: The discount rate is one of the most important assumptions in the funding valuation and plays a key role in assessing whether the pension plan has sufficient assets to meet its future pension obligations. It is used to calculate the present value of the future pension benefits that the plan expects to pay to members as well as the contributions it anticipates receiving.

The discount rate is a long-term assumption and takes into consideration interest rate trends, as well as provisions for plan maturity, risk tolerance and major adverse events.

Taking into consideration directional trends in observed real yields over the last three years and their potential translation into higher expected returns, the board decided to increase the real discount rate by 0.1% to 2.65% for the January 1, 2025 preliminary valuation. At the same time, as we continue to live in an uncertain and unpredictable investment and geopolitical environment, the real discount rate continues to reflect prudent provisions to navigate headwinds posed by the plan’s maturity, global economic challenges and an uncertain long-term outlook.

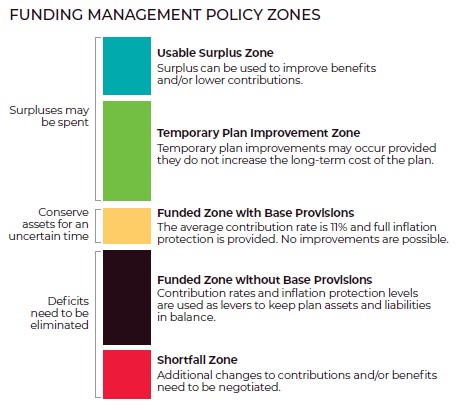

A: The FMP is an important document that provides the sponsors with a guidance framework for decision making when there is a funding surplus or shortfall. A key component in the FMP is the concept of funding zones, each defined by a range. The funding zones provide a point of reference for whether action is required by the sponsors and, if so, guidance is provided on how to use any surplus funds or resolve any shortfall.

Specifically, the FMP is used to determine when it is possible or necessary to increase or decrease benefits, lower or raise contributions, or simply conserve assets for an uncertain time. The FMP outlines preferred mechanisms associated with its various funding zones and it is ultimately the sponsors’ responsibility to decide which actions to take.

A: Shortfalls could happen in the future. However, financial levers available to the sponsors help manage the plan’s funding status. If needed, the sponsors can adjust benefits and/or contribution rates or utilize conditional inflation protection to keep the pension plan in balance.

That balance continues to be challenged by numerous factors including the plan’s member demographics, an uncertain and unpredictable investment and geopolitical environment, higher interest rates, climate change, and highly competitive investment markets. There can be no assurance of high investment returns in this complex and rapidly changing environment.

A: A future deficit could occur if assets are outweighed by liabilities on a future valuation date. Reserving surplus when a valuation is filed with the regulatory authorities makes it available for investing and earning returns, helping to protect the fund against future deficits. In other words, rather than being a cure, it is a preventative measure against future deficits.

A: Annual increases to pensions in pay are calculated by comparing the average Consumer Price Index (CPI) for the 12-month period ending in September to the previous 12-month average (the CPI Ratio). This approach smooths out short-term volatility and is similar to the approaches used by many large pension plans. The current levels of inflation will be factored into future increases to pensions as they flow into the averaging period.

The level of inflation protection provided to members is a plan sponsor decision. When the plan has a funding shortfall, smaller cost-of-living increases help to bring the plan back into balance. When there is a funding surplus, inflation levels may be partially or fully restored.

Pension credit earned before 2010 is 100% protected against inflation. Annual cost-of-living increases for pension credit earned after 2009 are conditional and depend on three factors:

1. Changes in the cost of living, as measured by the CPI Ratio as defined above.

2. The plan’s funding status, which is used to gauge how much of the CPI Ratio the plan can afford to provide.

3. When you earned your pension credit.Inflation Protection Levels

PENSION CREDIT | ALLOWABLE LEVELS* | CURRENT LEVELS* |

Earned before 2010 | 100% | 100% |

Earned during 2010-2013 | 50% to 100% | 100% |

Earned after 2013 | 0% to 100% | 100% |

*Percentage of the CPI Ratio.

The current 100% inflation level will remain in effect at least until the next funding valuation is filed with the regulators. A funding valuation must be filed at least once every three years.

---

IMPACT ON YOUR PENSION

To see how inflation increases affect your annual pension, register or sign in to your online member account.

A: Pension plan provisions can change over time and no generation of teachers has received the same benefits as the one before or after it. For example, inflation protection was not provided automatically until the mid-1970s, and many older members did not have an opportunity to retire at an 85 factor or receive a 10-year pension guarantee.

Keep in mind that Ontario’s Pension Benefits Act protects the value of pension benefits already earned by working and retired members.

MORE INFORMATION

Contact the Member Help Centre

Find out what three factors determine your annual inflation adjustment.