Global Investment Outlook: Watchouts and opportunities for founders

by Avid Larizadeh Duggan

A discussion with Edward Stanley, Executive Director of Research at Morgan Stanley, on the next 12 months and how startups can find opportunities in a time of economic slowdown.

At a glance

- Edward Stanley, Executive Director of Research at Morgan Stanley, shares his insights on finding opportunities in an economic slowdown.

- Uncertain times can produce opportunities for companies that understand their customers, make hard decisions quickly and have the flexibility in their business to remain funded through volatility.

- Although VC funds have amassed an estimated $530.8 bn in dry powder, as much as 20% of it may be earmarked for large infrastructure-type projects, particularly in the climatech space.

- The rule of 40 is a key metric to consider in this market, meaning the company’s revenue growth rate plus profitability margin should be equal to or greater than 40%.

Fundraising amid market uncertainty

So far, 2023 looks set to be another challenging year: the global economy is expected to slow, further interest rate hikes are expected and stock market volatility is likely to continue. Yet uncertain times produce opportunities for the best companies to shine –resilient teams who understand their customers and their pain points, who can make the tough decisions quickly, and who are able to create enough flexibility in their businesses to remain funded through the trough will emerge victorious.

I recently sat down with Edward Stanley, Executive Director of Research for Morgan Stanley, and our TVG community of founders, to discuss the essential steps founders need to take as they think about fundraising over the next 12 to 18 months. Here are my biggest takeaways from our discussion.

Don't be fooled by the illusion of excess dry powder

Last year saw venture capital firms continue to raise capital despite the market turmoil. By the end of the third quarter, VC fund managers had amassed $530.8bn of dry powder, an increase of 40.7% compared to December 2021, according to London, U.K.-based data and insights firm Preqin. However, we estimate that around 20% of this dry powder may be earmarked for infrastructure type investments, largely in the climatech space requiring large capital outlays for factories or carbon capture facilities for example. While another 20% is likely non-conventional capital, which appeared in the past two years and will be much slower to re-engage. That leaves around $200bn-$300bn of dry powder available to deploy into the market. For most of 2021 and the first half of 2022, unicorns were raising $20bn-$30bn per month, so there is a risk that founders could be left high and dry.

Copyright 2023 Morgan Stanley

Be cautious of the short-term market rally

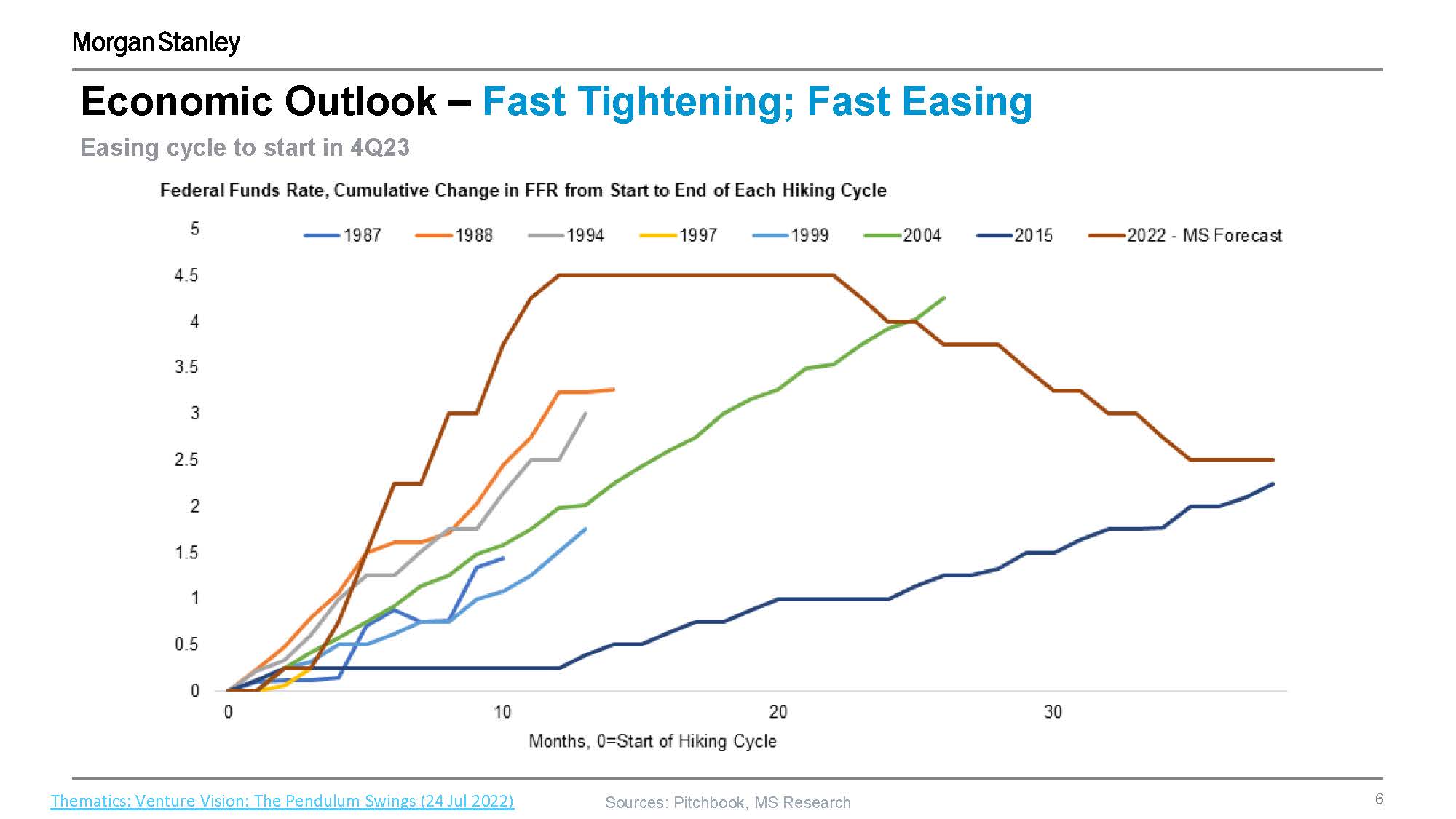

Stock markets have started 2023 on a positive note. The S&P 500 and STOXX Europe 600 are up nearly 8% year-to-date (as of 9 February) amid signs that inflationary pressures are starting to ease. Still, there are reasons to remain cautious. If we look at interest rate hiking cycles going back to 1987, the current cycle has seen the fastest and most aggressive monetary tightening by far. The Federal Reserve raised rates by 425 basis points between March and December 2022. Rates were increased by the same amount between 2004 and 2006, but over the course of two years rather than nine months.

Copyright 2023 Morgan Stanley

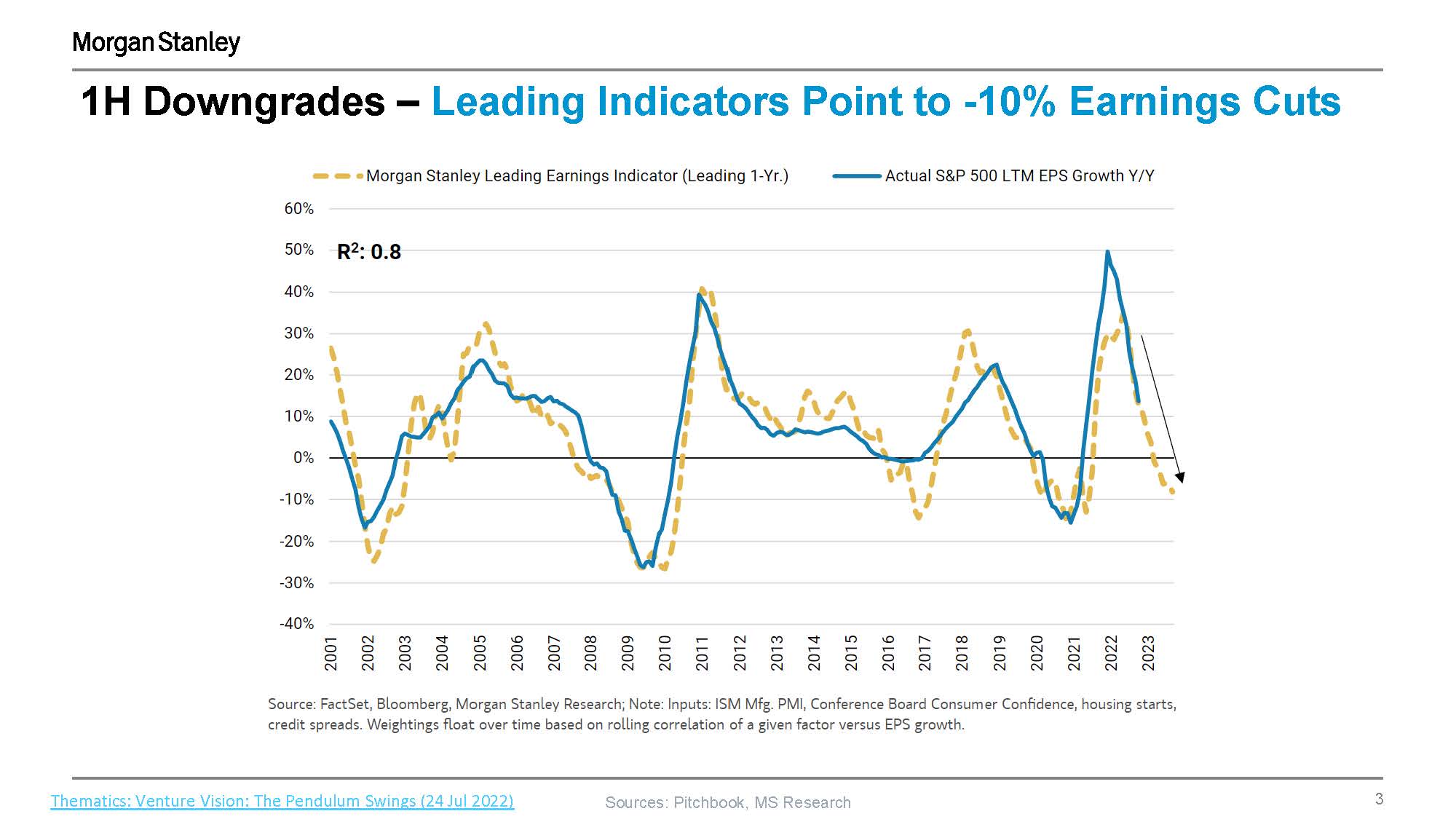

This unprecedented pace of interest rate hikes could lead to secondary and tertiary knock-on effects that we haven't yet seen. Leading indicators are falling fast, pointing to downgrades of 10%. So while the current rally is to be welcomed, it is likely to be short lived. The next six months won't be smooth sailing.

Copyright 2023 Morgan Stanley

Keep tech layoffs in context

Since the start of the year, 297 tech companies have laid off nearly 95,000 workers, and there are fears this number could surpass 900,000 by the end of 2023.

But the figures aren't quite as bad as they may seem. Companies such as Alphabet, Apple and Meta went on a hiring spree in late 2020, when economic conditions quickly improved following the initial Covid-19 crisis. The top 20 tech companies have now had to start cutting jobs, but these layoffs represent only 20% to 30% of incremental pandemic headcount additions.

The FAANGs – the Big Five companies: Meta (formerly Facebook), Apple, Amazon, Netflix, and Alphabet (Google) – still have much bigger workforces today than they did prior to the pandemic.

Take comfort from history

After a record-breaking 2021, the sharp slowdown in the global IPO market in 2022 was disheartening. But it's important to remember that markets move in cycles and there is light at the end of the tunnel. If we follow the 2008 trajectory, when the financial crisis put the brakes on the IPO market, we can expect markets to open up again in the third quarter. (ref slide 15)

If we follow that of 2000 – the dot-com bubble – markets will likely open up in the first quarter of 2024. In the interim, we will probably see a batch of good companies doing down rounds (i.e. companies selling shares at prices below their previous round's valuation) so they can IPO on an up round; this statistically leads to better long-term returns.

Expect more down rounds

With the global economy having taken a turn for the worse, it seems highly likely that we will see an uptick in down rounds this year. We are already seeing flat rounds with structured terms that favour new investors as if it were a down round.

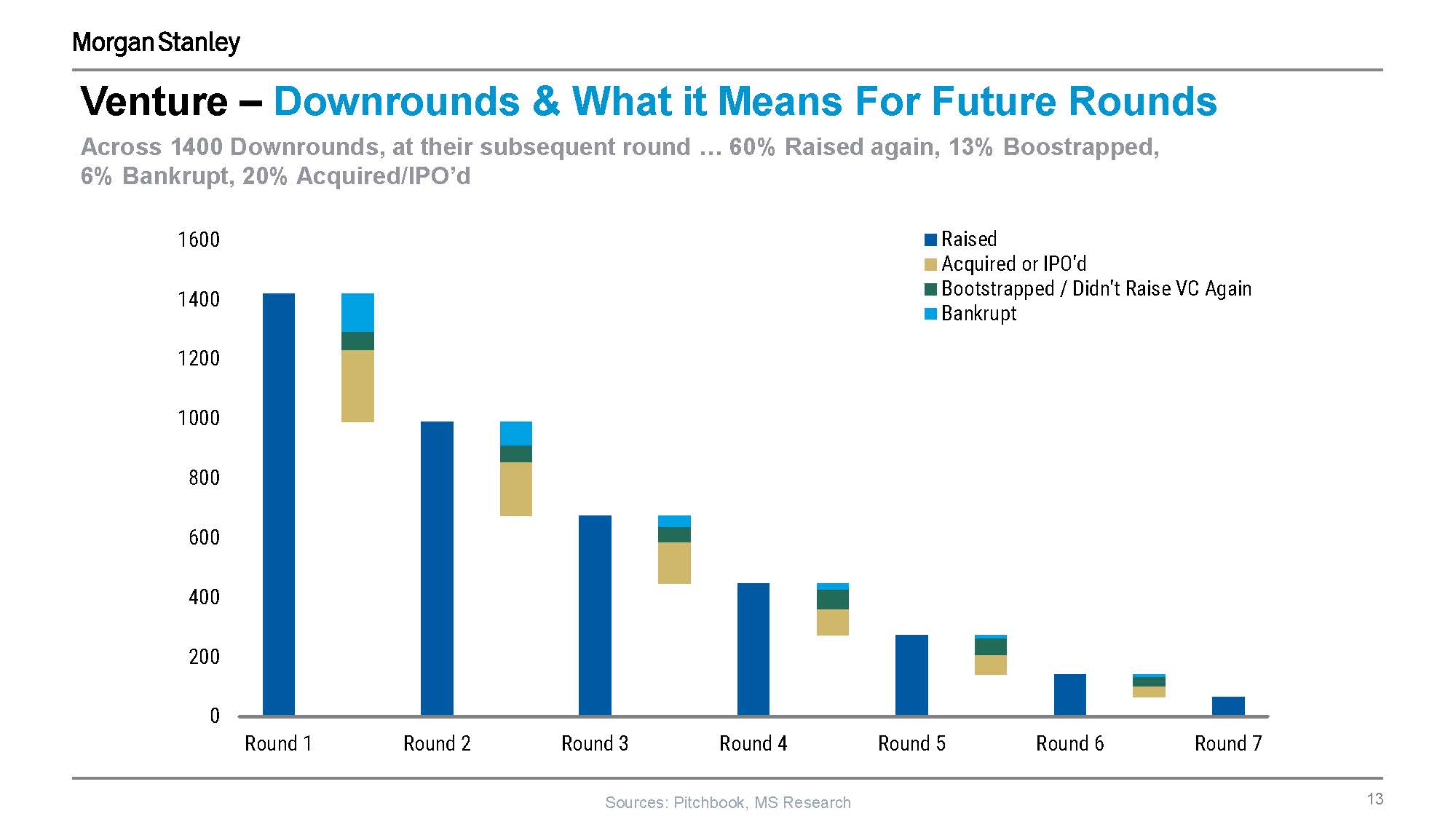

A down round is not the end of the world. An analysis of 1,400 companies found the bankruptcy rate was no higher for those who had agreed a down round than for those who hadn't. These companies are two times more likely to be consolidated by private equity versus seeing an IPO exit.

Copyright 2023 Morgan Stanley

In addition a clean down round can be a far better solution in the long term vs a convoluted structured round which creates misaligned incentives not only between investors and founders but across new and old investors depending on the type of outcome achieved.

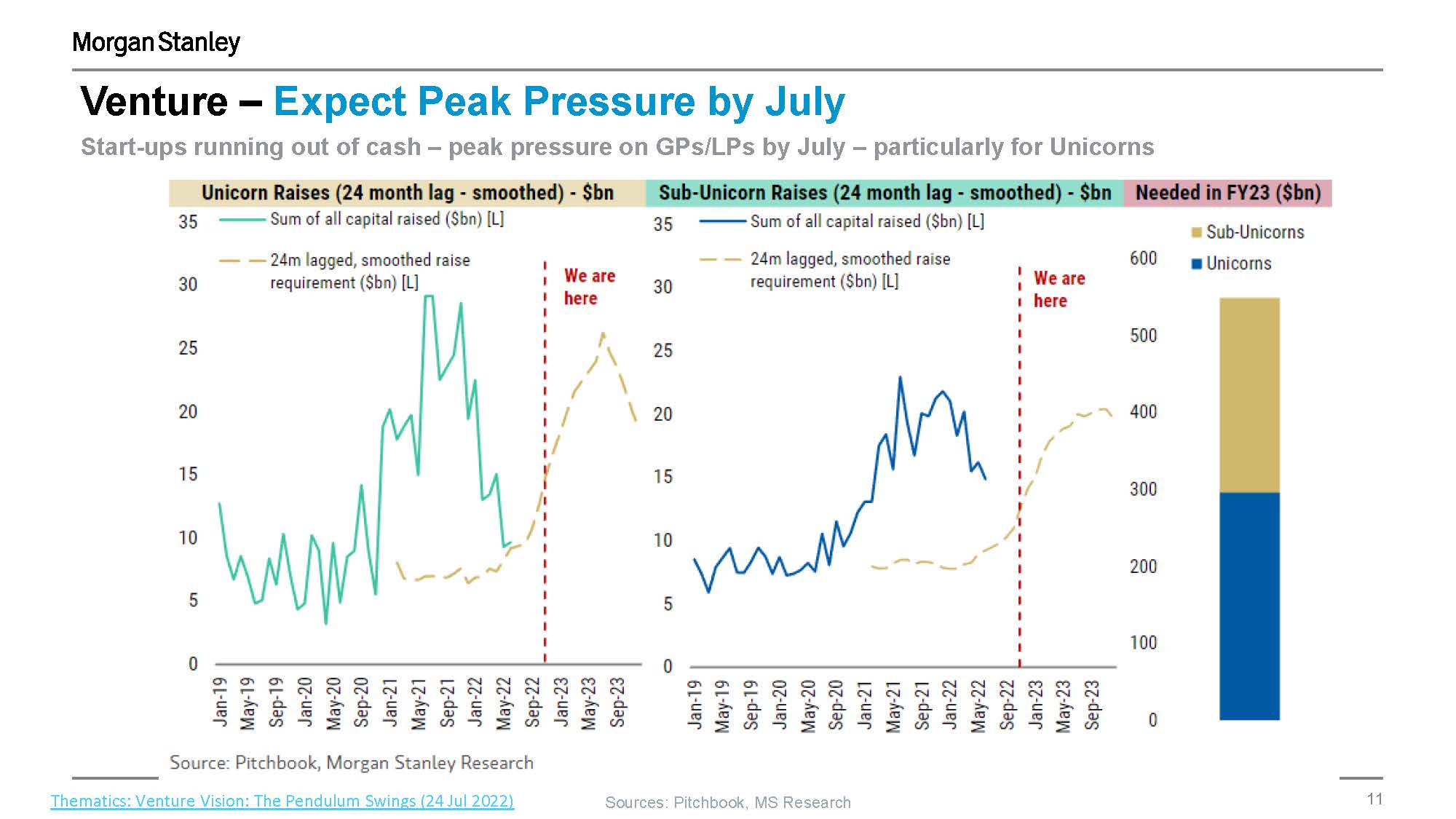

Prepare for peak pressure in July

The funding peak for the current cycle occurred in the fourth quarter of 2021. If we consider that most companies raise enough to give themselves 18 months before they need to start raising again, and then add another six to 12 months of runway extension, companies are likely to face peak fundraising pressure around July. Unicorns, in particular, will need to raise funds again after 24 months, even after cutting costs.

Beware high-interest loans

Venture debt can be a helpful way of bridging the gap until the next round of equity. But beware of credit offers taking advantage of the prevailing market uncertainty. There are currently short-term bridge loans charging interest rates of between 15% and 26%. Such high rates could lead to greater financial problems over the longer term.

Don't cut customer support

While some VCs will ask you to do the impossible – simultaneously extend the funding runway, cut burn drastically, get profitable, and maintain a healthy growth rate – one critical area which can help companies outstrip the competitors and boost their long-term strength is high quality customer service. It is invaluable to build customer loyalty during difficult times.

The Rule of 40 Dominates Public and Private Valuations

The rule of 40 is a key metric in this market. In other words, the company's revenue growth rate plus profitability margin should be equal to or greater than 40%. Public tech companies multiples are closely correlated to it. (ref slide 18) Recently, some investors have been looking even higher, to the rule of 60. As a fast growing innovative private technology company, you are not expected to be profitable from one day to the next. You are expected however to be building a business with long term sustainable unit economics, one in which you know what levers to pull to accelerate growth or increase margins and one in which you can demonstrate effective capital allocation.

Looking for an agile, global investment partner?

Find out about what Teachers’ Venture Growth can do for you.